Spiraling Towards Default

Spiraling Towards Default

Understanding contagion risks

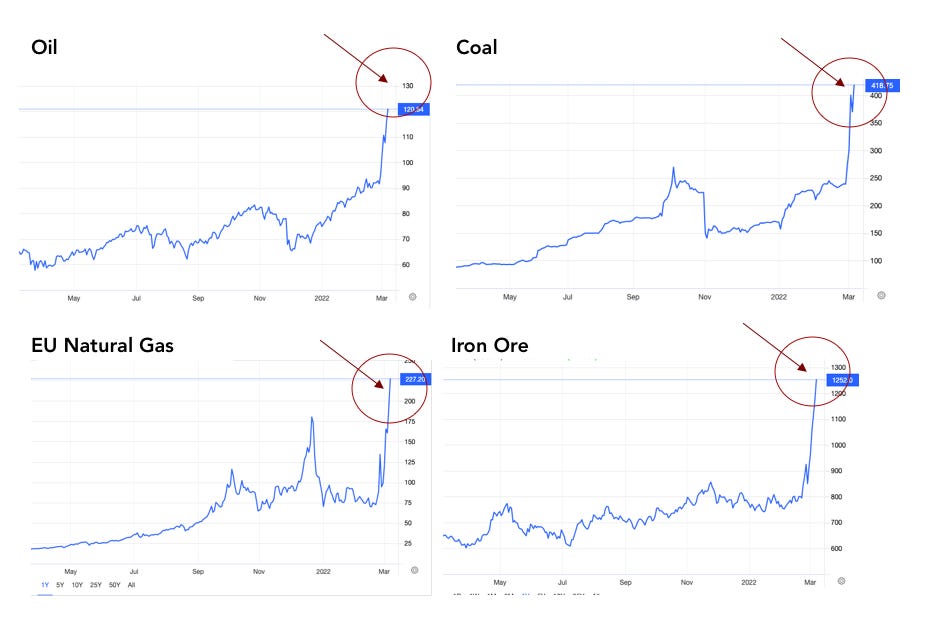

The Russia-Ukraine crisis is heating up even more. The U.S. has banned imports of Russian oil and natural gas, sending oil and gas prices to levels not seen in 15 years. Commodity prices in every area linked to Russian sanctions - oil, gas, coal, and iron ore included - are spiking, which will inevitably lead to even more severe inflation pressures around the world.

Currencies linked to economies heavily linked to Russian trade are also showing severe depreciation pressure. Hungry, Polish, and Czech currencies are falling against the U.S. dollar, which - combined with higher commodity prices - are sparking very real double-digit inflationary fears in these countries and inducing the region’s central bankers to intervene in markets and hike rates at a faster rate than previously anticipated.

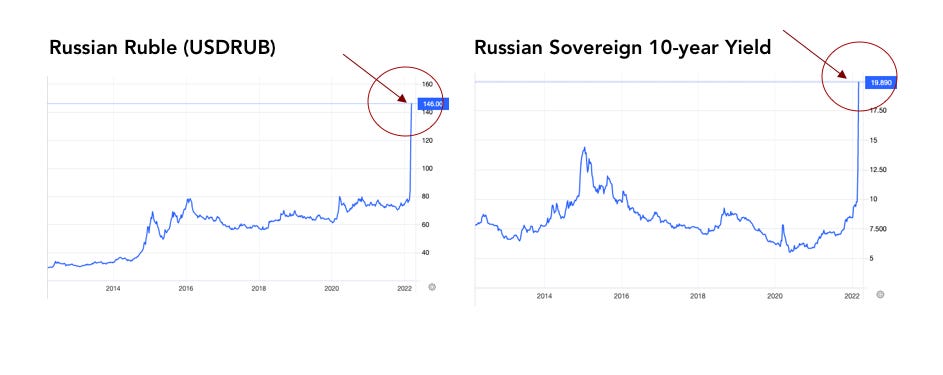

Meanwhile, the sanctions are proving to have a devastating blow to Russia’s economy. The ruble has now lost near 100 percent of its value over a month, while Russia’s 10-year sovereign yields have blown out to 20 percent. A rapidly depreciating currency can have devastating economic impacts on an economy, including spiraling inequality, rapid inflation (as imports become dramatically more expensive), bankruptcies (as companies cannot repay external debt or afford foreign inputs), and bank failures (as now a large swath of corporate borrowers cannot repay the bank).

It is only a matter of time before the average middle-class Russian family, as well as Russian corporations, feel severe pain from this war. And with Russia oil now banned in the U.S., the pain will be pushed onto Russian oil corporations, which will further pressure Putin to end the quagmire.

We see some evidence of middle-class Russians buying bitcoin and other digital currencies as a way of preserving their wealth. An interesting post from George Kaloudis from Coindesk shows that the volume of the BTC / RUB trading pair spiked to more than 240 percent above its 30-day trailing average in late February. However, in the context of crypto’s overall price action over the last six months, it is barely a blip.

Still, the ruble’s rapid depreciation will make it incredibly different for the Russian sovereign and Russian corporations to repay foreign creditors. President Putin recently signed a decree allowing it to repay foreign creditors in rubles, despite the contracts being written in USD. This could put Russia’s bonds into default.

And remember that markets hate defaults. They freakin’ hate’em.

Russian 5-year credit default swaps - a type of security that pays out in the event of a default - rose 50 percent this past weekend. JPMorgan estimates there have been about $6 billion worth of credit default swaps that bondholders have purchased on the back of Russia’s $40 billion in external debt that needs servicing.

The first test will be March 16 when two bond coupon payments will come due, although they each have 30-day grace periods.

A sovereign default will prove messy. As a recent WSJ article points out, when a country or corporation defaults on a bond with a credit default swap attached to it, usually investment banks or brokerages will hold an auction to determine the value of the debt, which usually will be offered at a steep discount to face value.

The insurance provider then must pay out the remainder of the face value of the debt to whoever bought the protection. But due to strict sanctions on Russia’s government debt, holding this auction may be impossible, further complicating the default process.

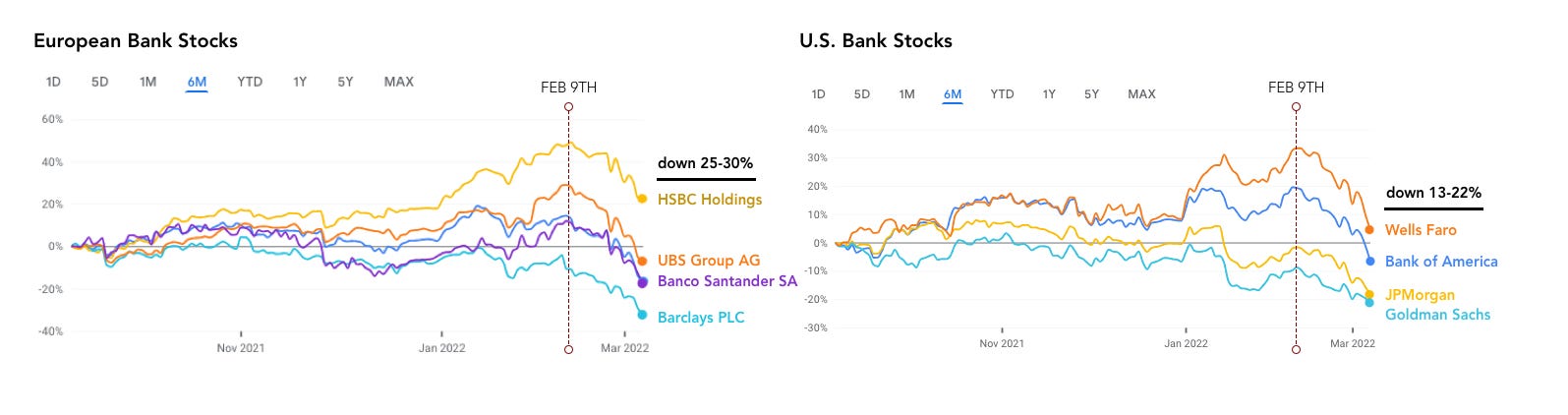

Meanwhile, European banks are expected to suffer pain as well. European banks are probably the most tradable asset that has the most direct exposure to Russian corporates and sovereigns. Since February 9th, European banks’ equity prices have dropped anywhere from 25 to 30 percent. European banks may have exposures either directly to Russian corporations or may hold collateral that is backed by Russian banks. Or, they issue loans to European companies that do trade with Russia.

Another victim of Russia’s invasion: German overnight collateral. As investors flee to safety, we’ve seen a shortage of available safe-haven German bond collateral in recent weeks. German bonds are the euro zone’s safest asset and are thereby used as collateral against overnight repurchase loans and securities lending in Europe’s overnight banking market (click here to understand what an overnight lending market actually is).

The crisis has boosted demand for sovereign bonds as use for collateral in creating short positions, which in turn has made the securities less available for collateral in the overnight market. The squeeze has been exasperated by Russian banks being cut off from the secondary market, which also holds these securities as collateral.

Disruptions in the overnight market have at times been the canary in the coal mine for larger-scale financial turmoil (i.e. the 2008 financial crisis), but so far we have not seen panic selling yet. Banks around the world learned their lesson after the 2008 financial crisis and - thanks to stricter regulations - have better capital buffers than before. Trading assets as a percentage of total assets for banks has been reduced thanks to post-2008 banking reforms. Banks have also increased their use of hedging derivatives to help alleviate volatility in their balance sheet. We do not see a full-blown contagion crisis emerging yet.

But make no mistake: pain will be felt around the world from this war.

Russia produces 10 percent of global oil and gas supplies and supplies 40 percent of Europe’s gas demand. Europe can’t meaningfully replace Russian gas until likely 2030 at the earliest, which means it will have no choice but to pay higher costs for energy.

And while the U.S. has the Defense Production Act, which enables it to increase energy capacity during defensive emergencies, even if the U.S. could increase oil drilling immediately, it would take six months for production to start from the time the oil is drilled. And in a country that has been adamant about transitioning away from fossil fuels, it’s unlikely oil companies will want to make this investment.

America and European allies seem ready to suffer the costs of this war, inflation and supply-chain woes be damned. The tide so far is on their side. Allies are likely to continue to supply Ukraine forces with armaments in search of either a full-blown collapse of the Putin regime or a slower weakening of Russia’s state capacity.

World support for Ukraine has been pronounced, and Ukraine is likely to continue its use of imaginative defense measures to wear down an already morale-deflated opponent.

While all sides will be weakened for their efforts, the key question is which side will weaken first.

Here’s my take on what happens next.

Making predictions in wartime is a fool’s game. And already, I’ve made mistakes on its outcome.

But from the evidence so far, the die seems cast.

Putin’s war has proven to go much worse than he thought. And his cabinet is likely going to do something about it.

There is ample evidence that even Russia’s top intelligence agency was not adequately informed about this war’s preparation. Many Russians do not support the war, even within the state’s highest levels (Putin’s own spy chief was seen on TV trying to maneuver himself out of a verbal support vote for the invasion).

Putin will likely try more extreme measures to get what he wants - cyber attacks, ramped-up attacks on civilians, or potentially even limited strikes against allies that encroach too closely towards the battle’s front lines.

But sooner or later, the pressure from the oligarchs and his people - as a result of intense economic pressures - will induce him into negotiations.

Otherwise, the Russian state could collapse. And the ramifications of that could be much worse.

Disclaimer: BubbleCatcher is published as an information service for subscribers, and it includes opinions as to forecasts on the global economy and its impact on securities linked to economic activity. The publishers of BubbleCatcher are not brokers or investment advisers, and they do not provide investment advice or recommendations directed to any particular subscriber or in view of the particular circumstances of any particular person. BubbleCatcher does NOT receive compensation from any of the companies featured in our articles. At various times, the publisher of BubbleCatcher may own, buy or sell the securities discussed for purposes of investment or trading. BubbleCatcher and its publishers, owners, and agents are not liable for any losses or damages, monetary or otherwise, that result from the content of BubbleCatcher. Past results are not necessarily indicative of future performance. The information contained on BubbleCatcher is provided for general informational purposes as a convenience to the subscribers of BubbleCatcher. The materials are not a substitute for obtaining professional advice from a qualified person, firm, or corporation. Consult the appropriate professional advisor for more complete and current information. BubbleCatcher makes no representations or warranties about the accuracy or completeness of the information contained on this website. Any links provided to other server sites are offered as a matter of convenience and in no way are meant to imply that BubbleCatcher endorses, sponsors, promotes, or is affiliated with the owners of or participants in those sites, or endorses any information contained on those sites unless expressly stated.