NGO

As expected, the Russia - Ukraine border is heating up. The previous and seemingly remote possibility last month that Russia would dare invade Ukraine is now looking likely.

Putin is not crazy, as I explain below. In fact, he’s making a very rational if risky move, in part fueled by his declining popularity at home. But it’s a move which the west will admittedly struggle to mount an effective response to.

First, Putin is likely to continue to find creative ways to create legitimacy for invading Ukrainian territory. Putin has recently said he “recognized” Russian separatist-held regions. By recognizing their sovereignty, this now gives Putin the pretense to send troops to these regions for “peacekeeping.” And we see signs that this could just be beginning.

For instance, Russia has been evacuating women and children from Russia-held areas for the last few weeks. There are also reports of Russia already engaging in grey-zone warfare tactics (as reported on by the NY Times in their “Daily” podcast here) such as intentionally creating flare-ups and then using them as a pretense for sending troops in, as well as initiating cyber-attacks against Ukrainian government websites and banks.

Be prepared for a drawn-out conflict that involves multiple types of grey-zone tactics and operations. Putin’s popularity has been waning in Russia, so the timing works well for him. Moreover, the American military’s morale has been severely damaged by what happened in Afghanistan, while the American public is exhausted from covid and still reeling from supply-chain bottlenecks that will likely wreak havoc on the domestic economy for at least another few years.

Meanwhile, European allies desperately need heating fuel for the winter, particularly with natural gas prices already sky high, and will not easily tolerate oil or natural gas sanctions. These conditions help splinter NATO-member interests, inviting the perfect opportunity for Putin to spark a conflict where he doesn’t want interference.

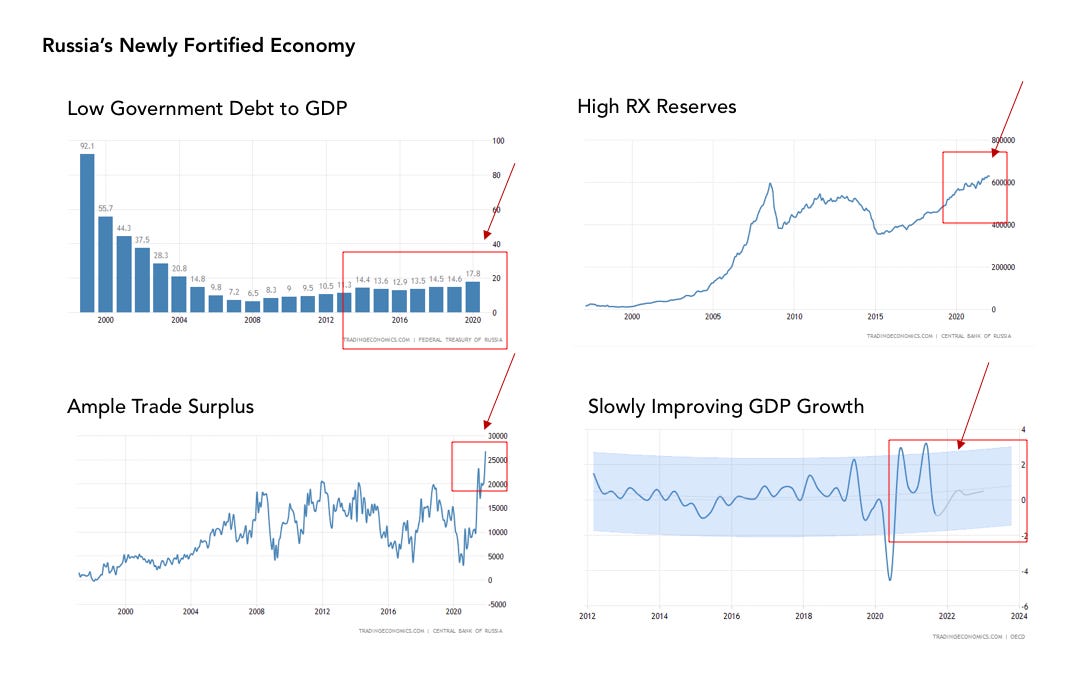

Russia’s economy is - relatively speaking - better positioned to deal with financial sanctions. Government debt is low and not heavily reliant on external financing. Russia’s FX reserves are some the highest in the world at $630 billion, in part due to its massive trade surplus. Russia is a net exporter of oil and gas, so its economy is not as sensitive to high commodity prices as many western countries.

It also is a major exporter of critical commodities such as copper, aluminum, and wheat, which importing countries will struggle to supply if sanctions are put in place. Russia just signed a 30-year natural gas deal with China via a new pipeline, with both countries agreeing to settle transactions in euros to diversify away from dollars. And while overall GDP growth rates have been volatile, the trend is improving. Finally, Russian leadership has helped domestic industries supply products that previously came from imports.

Putin’s moves will likely be measured at first. Putin is best known as a politician who takes measured risks. He is unlikely to attempt first take over the entire Ukraine all at once, but instead, just focus on lower-risk regions such as the Russian-dominated Donbas region and Crimea regions. If these moves prove successful, more territory may be at stake.

In addition to ground-troop operations that could get violent and ugly, we should expect Russia’s government will continue to engage in grey-zone warfare tactics, which will make it difficult for democratically-led countries to respond. This will include things like:

staged “attacks” on Russian forces that will create a legitimate reason for Russian battalions to use force against Ukrainians

denial and deception operations that conceal or obfuscate the presence of Russian forces in Ukraine (i.e. sending troops in without clear insignia)

efforts to conceal Russia’s true objectives in the conflict, so as to persuade their own citizens as well as others that their aims are reasonable, limited, and acceptable

retaining plausible legality for their actions by changing conditions on the ground so that they are perceived to be engaging in operations that Western countries have done in the past (i.e. Kosovo in the 1990s, the invasion of Iraq in 2003)

concerted efforts to shape the narrative around the Ukrainian conflict to their favor, such as couching the Ukrainian government as illegitimate or corrupt

cyberattacks on key infrastructure both in Ukraine and against NATO allies

While the currency and bond markets are punishing the nation’s currency and sovereign bonds, we are not yet at panic levels. Even if we were, Russia is more prepared than ever to cut itself off from foreign financing sources and rely on domestic financing. Moreover, a weaker currency just makes a net exporter’s goods cheaper on global markets. And if they want to reverse the currency’s trend, they have a $600 billion war chest to intervene with.

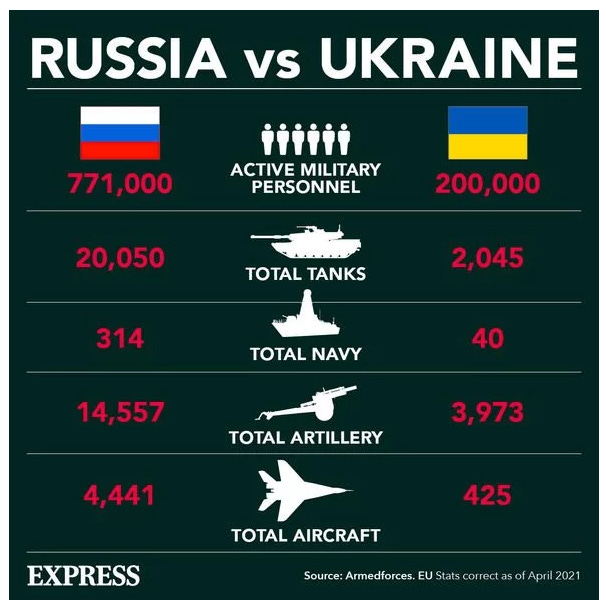

While Ukraine could put up a fight, they do not have the military hardware or numbers to mount a significant defense. From a strict hardware perspective, it is unlikely that Ukraine will be able to mount a significant defense. Russia has one of the largest militaries in the world.

The bigger question is what a Russian siege would look like. Modern history has proven how difficult urban-area sieges are for occupying countries. This could prove Russia’s weak point and one that the west could offer Ukraine the most support and leverage on.

NATO allies will need to stand united and be resolute to act as an effective deterrent, even though the more severe sanctions will hurt them, too. Sanctions on Russian banks, blocking the servicing of Russian sovereign debt, preventing Russia from purchasing high-end semiconductors, targeted sanctions on oligarchs, and even removing Russia from the SWIFT financial system are measures NATO allies have at their disposal.

Blocking Russian banks from U.S. dollar transactions would be the most brutal blow and would effectively block Russian businesses from doing business abroad. Even the country’s ample FX reserves could not shield Russian companies from such a move. Still, such moves will have costs: European businesses with strong ties to Russian suppliers will feel the sting as well, which will end up fraying the resolve of NATO allies.

Still, for the moment, the long-term political gains of reclaiming lost Russian territory outweigh the short-term costs sanctions might have on his and his cronies’ wealth.

The global market reaction will likely be added volatility over the short term. Equity prices will likely fall further and stay sluggish for months. Higher oil and gas prices will not significantly dampen U.S. growth prospects, but the risk premium attached to a nuclear power invading a NATO “enhanced opportunity partner” risks a doomsday scenario that will weigh on market sentiment.

Remember too that Russia is a major net oil exporter, producing 10 percent of the world’s oil supplies and supplying one-third of Europe’s natural gas needs. Knocking that much supply offline would be a major event. Rising oil prices will likely filter through other commodity prices as well, which will further create pressures on supply chains and add to inflationary pressures around the world. Oil producers outside of Russia could be beneficiaries, while companies with high exposure to Russian revenues could be hit.

Large-scale cyberattacks against U.S. companies or infrastructure could also cause disruption.

Rising Russian sovereign bond yields will also likely occur, but further currency depreciation is not a certainty. Russia’s large surplus reserves could act as a deterrent for would-be speculators.

Longer-term, other countries will likely be looking at this incident carefully. Russia’s aspirations for reclaiming Ukraine look eerily similar to the way many other countries eye land beyond their territories: China towards Taiwan, Israel towards Palestinian territories, North Korea towards the South. What will America’s response be? Will it be able to rally NATO allies? Will the response prove effective? You can be sure that whatever direction this goes, the ramification of its results will be heavily scrutinized behind closed doors.

A failed response by America here could be a harbinger of what the 21st century will look like without a strong Democratic superpower.

Disclaimer: BubbleCatcher is published as an information service for subscribers, and it includes opinions as to forecasts on the global economy and its impact on securities linked to economic activity. The publishers of BubbleCatcher are not brokers or investment advisers, and they do not provide investment advice or recommendations directed to any particular subscriber or in view of the particular circumstances of any particular person. BubbleCatcher does NOT receive compensation from any of the companies featured in our articles. At various times, the publisher of BubbleCatcher may own, buy or sell the securities discussed for purposes of investment or trading. BubbleCatcher and its publishers, owners, and agents are not liable for any losses or damages, monetary or otherwise, that result from the content of BubbleCatcher. Past results are not necessarily indicative of future performance. The information contained on BubbleCatcher is provided for general informational purposes as a convenience to the subscribers of BubbleCatcher. The materials are not a substitute for obtaining professional advice from a qualified person, firm, or corporation. Consult the appropriate professional advisor for more complete and current information. BubbleCatcher makes no representations or warranties about the accuracy or completeness of the information contained on this website. Any links provided to other server sites are offered as a matter of convenience and in no way are meant to imply that BubbleCatcher endorses, sponsors, promotes, or is affiliated with the owners of or participants in those sites, or endorses any information contained on those sites unless expressly stated.

Really insightful and practical analysis, very well done and something we investors need to appreciate. Thanks.

Amazing rundown, but I’d expect nothing less from you. Keep up the great work, Greg.