Financial Wars

Over the past week, news on Russia’s invasion of Ukraine has been updating at a furious pace. Tensions have ratcheted up faster than expected, suggesting this war could take twists and turns far beyond the boundaries of what we had originally expected.

Russia’s violent incursions into the country’s center, including Kiev, have been faster and more violent than anticipated. Meanwhile, Ukrainian forces have put up a stronger fight than expected as well, slowing Russia’s advance.

Russia’s initial plan to quickly overwhelm Ukraine forces with minimal casualties has been stopped dead in its tracks, and it looks like they will need to ramp up their offense soon as a way to stem casualties on their own side.

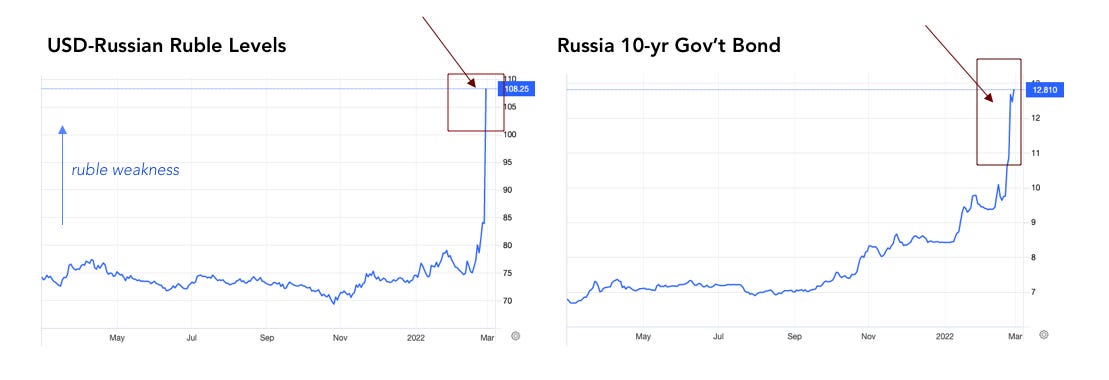

Meanwhile, U.S. authorities in turn have also been ramping up sanctions against Russia faster than anticipated, causing dramatic moves in the country’s financial markets. The Russian ruble has plummeted 40 percent over the last two days while the country’s sovereign bond yields have skyrocketed to 12.8 percent.

The dramatic moves on Russia’s currency and bond yields suggests the sanctions being enacted will induce a massive bite. In a bold move, the U.S., E.U., Canada, and the U.K. have issued bans of their firms from transacting with the Russian central bank, foreign ministry, and sovereign wealth fund.

This type of sanction is much stronger than simply cutting off Russian banks from the SWIFT network, as I explain below.

Messing with a country’s FX reserves is akin to financial warfare. Russia’s central bank has a whopping $640 billion in foreign exchange (FX) reserves, which is a huge figure and one of the largest in the world. But a good chunk of these assets are not held in Russia.

Roughly $400 billion is held in custody in investment banks in major cities around the world like New York, London, Berlin, Paris, and Tokyo or held at foreign institutions like the IMF and BIS.

Under normal times, if the ruble were to suddenly depreciate, the central bank could simply sell these FX reserve assets (usually invested in U.S., European, and Chinese sovereign debt) and then buy up their domestic currency in a move called an “intervention.”

However, freezing Russia’s assets abroad dramatically cuts down the central bank’s resources for fighting currency depreciation, as the figure below illustrates.

That all said, from the image above, we can still see Russia’s central bank is far from out of ammunition. Russia still has about $140 bn worth of domestic gold reserves, $84 bn in Chinese bonds, $12 bn in cash, and $268 bn worth of assets it could strong-arm from its citizens and local businesses.

Historically speaking, this should be enough ammunition to last for multiple days or even weeks against depreciation pressure. But how the market perceives this will be key in upcoming weeks. And so far, the signs do not look encouraging.

Russia is already shoring up domestic, non-reserve assets to combat further depreciation. Already, we see Russian monetary authorities have ordered Russian exporters to sell 80 percent of their FX revenues on the market to make them available. They also have hiked interest rates to an eye-popping 20 percent from 9.5 percent previously, all as a way to stop citizens and companies from exchanging their rubles into foreign currency, sparking capital flight and thereby exasperating the ruble’s fall.

They have also ordered brokers to suspend short-selling in the Russian market, as well as stopping foreign entities from selling Russian securities.

Still, this all might not be enough. A 40 percent depreciation is serious business, with potential long-term ramifications being rapid inflation (as imports become prohibitively expensive), numerous corporate failures, and potential social stability risks.

Should this continue, corporations will struggle to roll over debt due to higher interest payments, and importers could go under as they fail to find substitute products at a reasonable rate.

Aggregate investment could plunge, throwing the economy into a recession. Rating agencies have already taken note, with S&P recently lowering Russia’s foreign currency rating to BB+, while ruble rates on the black market have skyrocketed even further to 152 / $ this past weekend.

Russia’s central bank may be forced to recapitalize banks and large firms with significant exposures, and printing rubles may be the only way to do it, further depreciating the currency.

Longer-term impacts of these moves:

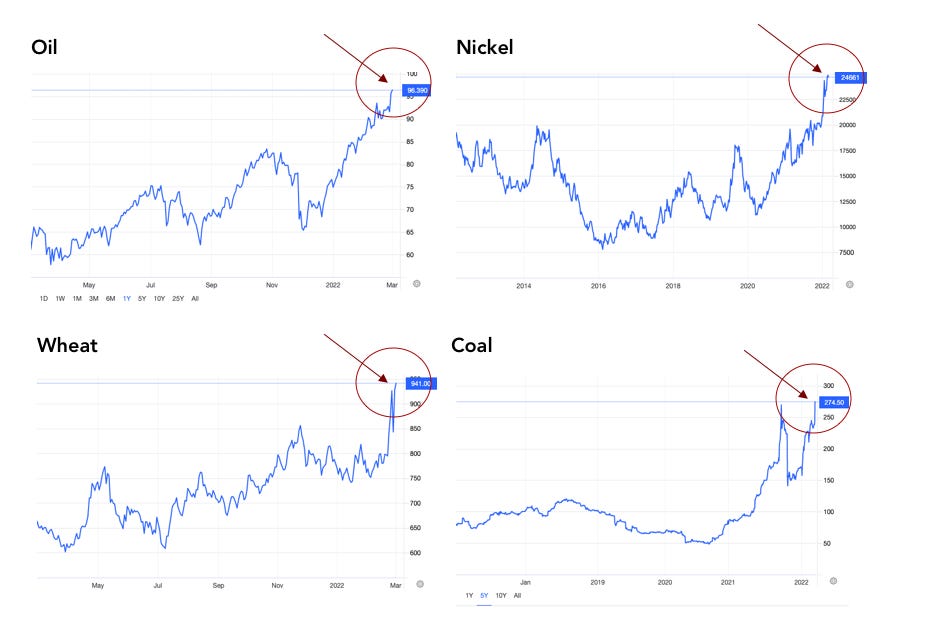

further surges in commodity prices, particularly oil, gas, grain, nickel, coal, steel and wood, all which Russia is a major exporter of. Already we’re seeing these prices jump higher, and further moves should be expected unless we see a breakthrough in negotiations.

countries further diversifying away from U.S. dollars. Central banks are watching these moves closely and seeing the potentially negative effects of having their reserves denominated in dollars. China in particular may make major moves to further diversify away from dollars, as they may want to make their own moves against Taiwan in upcoming years and not want to face the same risks as Russia is now.

the crystallizing of a new front for warfare. The U.S. has used sanctions against Russia before (2014), but the breadth and scope of today’s sanctions is more severe. Financial warfare works, as the last few days, have proven, and countries are likely going to respond to further insulate their assets from America’s control, or potentially create their own methods for enacting leverage against the U.S. dollar themselves.

Disclaimer: BubbleCatcher is published as an information service for subscribers, and it includes opinions as to forecasts on the global economy and its impact on securities linked to economic activity. The publishers of BubbleCatcher are not brokers or investment advisers, and they do not provide investment advice or recommendations directed to any particular subscriber or in view of the particular circumstances of any particular person. BubbleCatcher does NOT receive compensation from any of the companies featured in our articles. At various times, the publisher of BubbleCatcher may own, buy or sell the securities discussed for purposes of investment or trading. BubbleCatcher and its publishers, owners, and agents are not liable for any losses or damages, monetary or otherwise, that result from the content of BubbleCatcher. Past results are not necessarily indicative of future performance. The information contained on BubbleCatcher is provided for general informational purposes as a convenience to the subscribers of BubbleCatcher. The materials are not a substitute for obtaining professional advice from a qualified person, firm, or corporation. Consult the appropriate professional advisor for more complete and current information. BubbleCatcher makes no representations or warranties about the accuracy or completeness of the information contained on this website. Any links provided to other server sites are offered as a matter of convenience and in no way are meant to imply that BubbleCatcher endorses, sponsors, promotes, or is affiliated with the owners of or participants in those sites, or endorses any information contained on those sites unless expressly stated.