Blood in the Streets

The tech market is undergoing a blood bath that hasn’t been experienced in over a decade. It’s ugly.

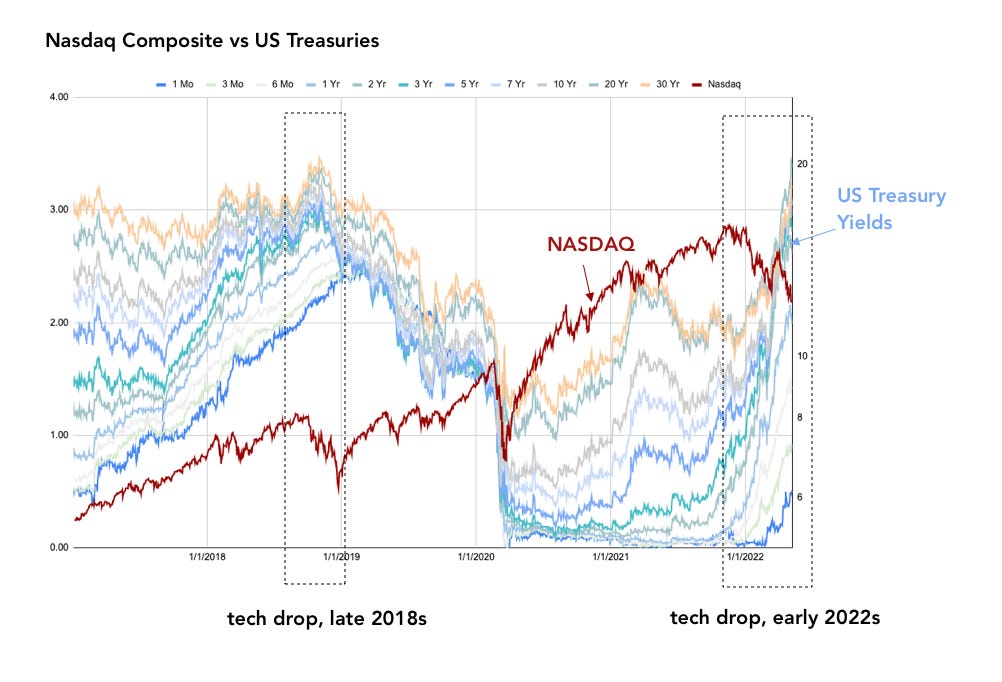

The primary culprit on the surface seems to be simple: inflation. Inflation fears are contributing to a rise in the perception that the Fed will raise rates further. Which in turn is contributing to yields rising across the board, most pronounced in the 10- through the 30-year range.

On the face of things, we have a perfect confluence of factors that seem to be glaring down on the Fed now. Things like lingering covid supply-chain woes, commodity price hikes linked to the Ukraine-Russia conflict, and a general sense of gloom and doom in market sentiment.

But are these factors really that bad? Oftentimes, the market makes highly reactive moves to the market sentiment that is beyond what the data suggests. So let’s take a look at the data.

From the above pix, we can see that interest rates indeed are rising quite high. Yes, this is a problem, and yes, all things equal, this will contribute to declines in the valuations of all companies, but most particularly, high-flying tech companies.

But is this sudden fear warranted? In other words, are commodity prices rising in synch? Is inflation broad-based? Will the Fed’s reaction thereby require a jump into a recession?

Well, if inflation is supply-chain linked, maybe not. Commodity prices seem to actually be steadying a bit, with copper prices seeing in fact a dramatic decline. Even lumber prices, which previously were contributing to rapid rises in housing gains, seem to finally be steadying, in sharp contrast to their rapid price increases seen earlier in the year. This suggests the housing market may be in for an adjustment in the near future.

But what if inflation were demand-focused? What if the Fed just printed too much money over the last decade, and now this money has entered the hands of the U.S. consumer? Expectations of future inflation take hold, and now the Fed has to tackle the psychology of investors?

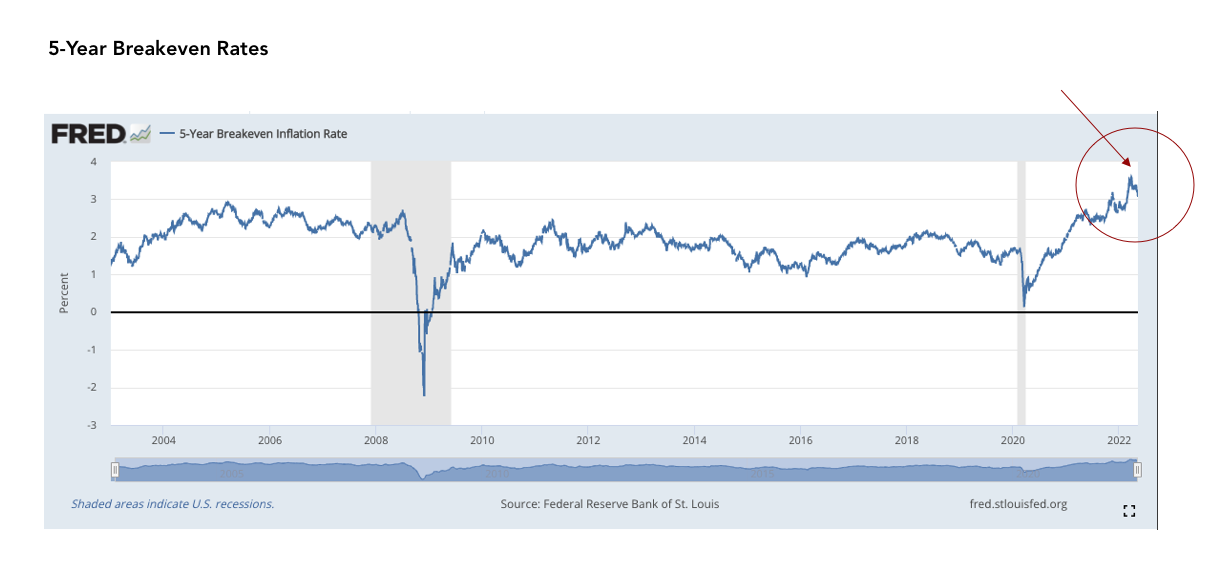

Even here, it’s hard to get a firm grasp on a story. We can measure demand-side inflation by looking at the 5-year TIPS / Treasury breakeven rates, which is simply the difference between the 5-year Treasury and the 5-year inflation-indexed security rate. And while this rate is indeed high, it’s actually beginning to decline relative to recent highs.

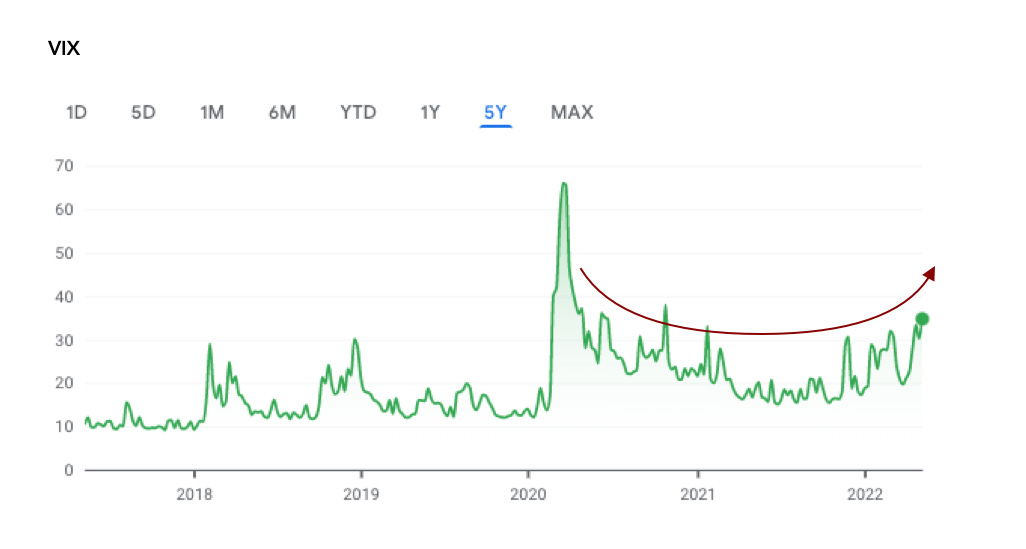

In the absence of clear data linked to actual economic evidence, we are left with the simple idea of market risk. Perhaps the market seems to be highly uncertain about which way geopolitics will go. Will the Russia-Ukraine conflict worsen and ensnare all of NATO? Yes, market volatility measures seem to be escalating …

… but this volatility doesn’t seem to be linked to the health of the Russian economy. Both the Russian ruble and 10-year yield seem to have improved dramatically over the last few weeks.

So in short, the market is skittish. Future global growth prospects, and the potential for a stagflation scenario, seem to be a contributing factor.

We’ll have to see where this goes from here to get a fuller view.

Disclaimer: BubbleCatcher is published as an information service for subscribers, and it includes opinions as to forecasts on the global economy and its impact on securities linked to economic activity. The publishers of BubbleCatcher are not brokers or investment advisers, and they do not provide investment advice or recommendations directed to any particular subscriber or in view of the particular circumstances of any particular person. BubbleCatcher does NOT receive compensation from any of the companies featured in our articles. At various times, the publisher of BubbleCatcher may own, buy or sell the securities discussed for purposes of investment or trading. BubbleCatcher and its publishers, owners, and agents are not liable for any losses or damages, monetary or otherwise, that result from the content of BubbleCatcher. Past results are not necessarily indicative of future performance. The information contained on BubbleCatcher is provided for general informational purposes as a convenience to the subscribers of BubbleCatcher. The materials are not a substitute for obtaining professional advice from a qualified person, firm, or corporation. Consult the appropriate professional advisor for more complete and current information. BubbleCatcher makes no representations or warranties about the accuracy or completeness of the information contained on this website. Any links provided to other server sites are offered as a matter of convenience and in no way are meant to imply that BubbleCatcher endorses, sponsors, promotes, or is affiliated with the owners of or participants in those sites, or endorses any information contained on those sites unless expressly stated.