Biden's Follies

Biden's Follies

... and the unraveling of the Democrats' hopes for 2024

As economic data comes out, we are finally beginning to see how damaging the Biden administration’s pandemic relief package has been to our economy.

With the most recent U.S. inflation data printing at over 8 percent and well above expectations late last week, the market is now caught trying to guess how many more rate hikes will be needed. Unfortunately, there seems no upper limit in sight. Inflationary pressures remain high, show no signs of abating for the foreseeable future, and will likely be the defining event of the downfall of Biden’s presidency. Keep reading to figure out why.

The Fed has a two-day meeting this week with a decision on rate increases being released this Wednesday at 2 pm. Given last Friday’s inflation release, it’s becoming increasingly likely it will have to bump its anticipated rate hike from 50 to 75 basis points. And we may just be at the beginning of the Fed’s rate hike cycle.

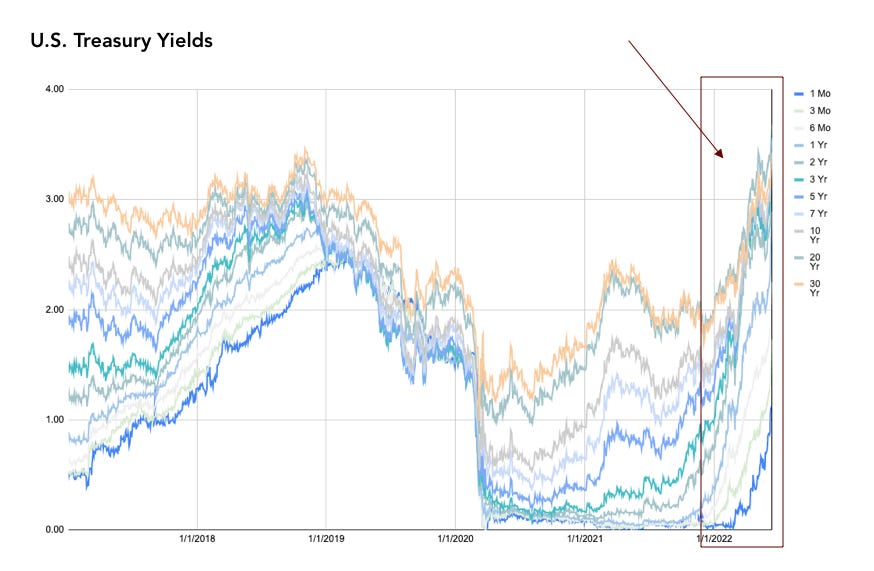

The effects of these pressures are multifold. U.S. Treasury yields continue to rise at a rapid clip, with late last week showing a significant bump as a result of the inflation print. The upwards pace shows no signs of stopping. We also see at the upper ranges of the yield curve (2-10 years) a bit of “yield inversion” where shorter-dated yields accelerate past longer-dated yields. This suggests an upcoming recession may be becoming priced in by markets.

Although economists are known for being wrong (as they were forecasting the inflation blowout we’re having), seven out of 10 polled by the Financial Times and the University of Chicago suggest the U.S. will enter a recession either in the first or second half of next year (2023).

Meanwhile, the U.S. dollar has responded by appreciating sharply against major currencies. Investors continue to sell European and Japanese bonds and buy U.S. Treasuries to take advantage of the yield differential between the two regions, putting upwards pressure on the currency. We are now at the dollar’s highest level in nearly 20 years, a bad sign for U.S. corporate profits who sell overseas and will see their foreign-currency-denominated profits sink like a stone.

The U.S. consumer is also feeling a massive hit right now. Consumer sentiment in the U.S. is at its lowest level ever recorded. 46 percent of consumers attributed their negative views to inflation, the biggest share since 1981 (when stagflation was also an issue). The warning bells from CEOs about an upcoming recession don’t help either.

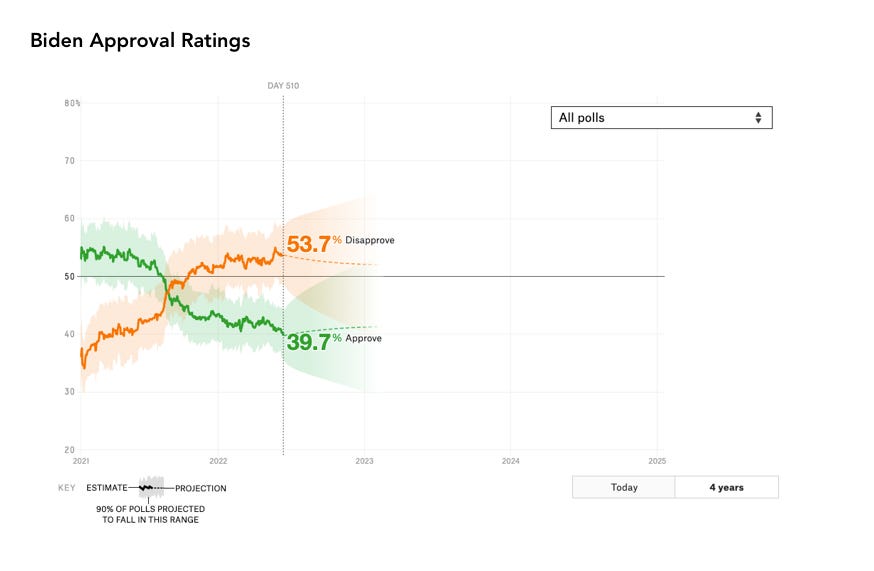

Meanwhile, Biden’s approval rating has dropped to its lowest level ever. Given how bad inflation is in the U.S. relative to the rest of the world, the U.S. has no one to blame but itself for its woes. The Wall St. Journal wrote an excellent piece on what went wrong with fiscal policy during the pandemic. The short of it? The administration was fighting the last war (the financial crisis of 2008) by enacting a massive stimulus that was too big for the economy to handle.

Meanwhile, the other sources of inflation - the Russian-Ukraine War and resulting price hikes in oil and wheat - show no signs of abating. Oil is at its highest level in decades, and wheat prices still remain elevated. Prices for these commodities are likely to remain high as the war continues.

The problem now, of course, is that the Biden has only two years to recover from this fiscal disaster before the next election. And given how long it can take for an economy to recover from either rapid inflation or a resulting recession - anywhere from two to four years at best - the U.S. public will not have any patience for an administration that got it so wrong.

And the fact that he shows no signs in alleviating these pressures, such as offering to help broker a peace deal between Russia and Ukraine, suggests that this inflationary pain will linger for the rest of his term, spelling near certain doom for the Democrats hopes in 2024.

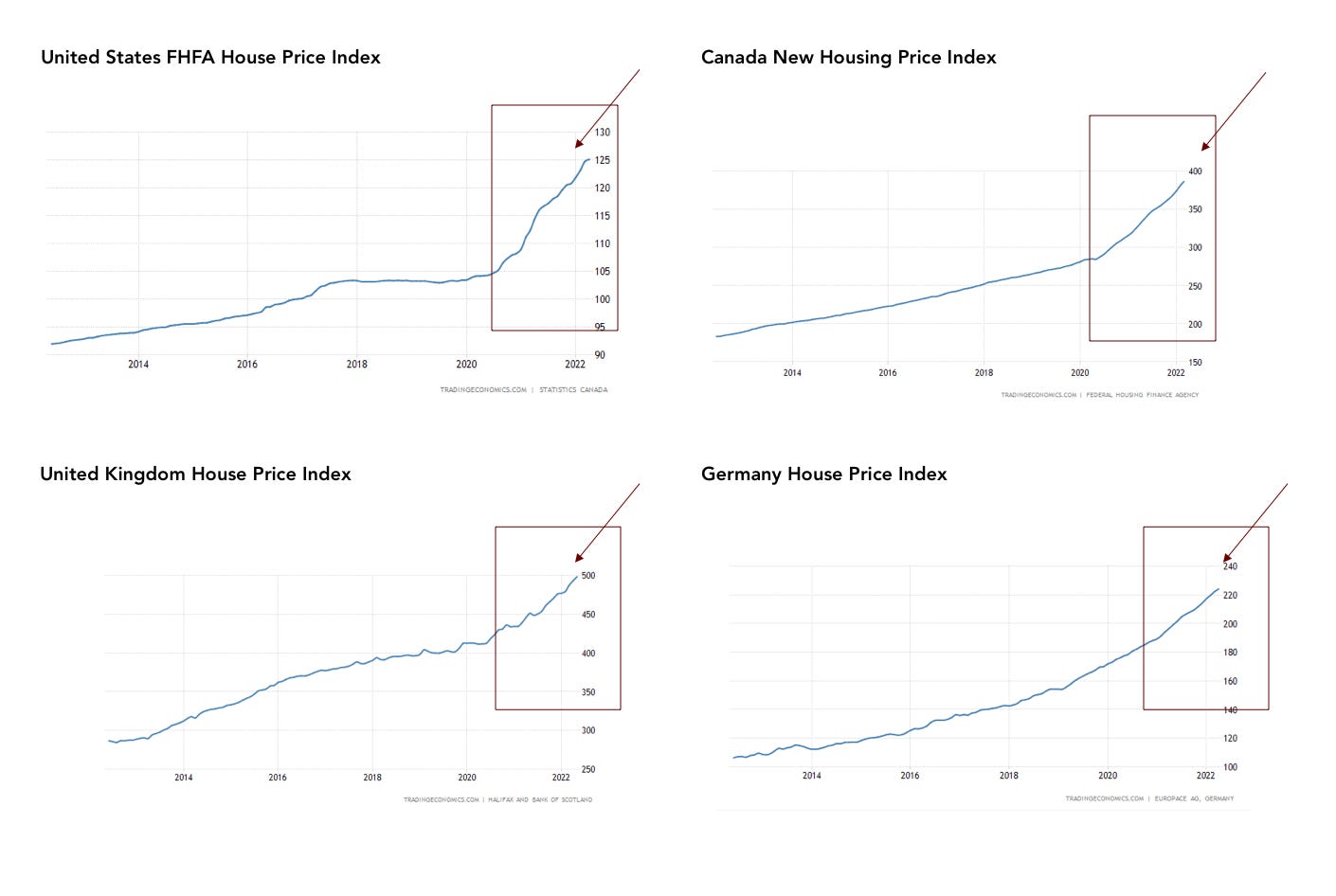

Nor do the Democrats seem to be addressing the other major elephant in the room: the housing affordability crisis in the U.S. This is a growing problem in major democracies around the world, but a glance at the most recent data shows just how insane price increases have been in the U.S. relative to other countries. Since Democrats tend to be younger and live in the expensive coasts, they are the ones most impacted by the housing affordability crisis. The Democrats’ inaction on this front - or, as some could reasonably argue, direct contribution to the crisis - could likely be the nail in the coffin for their hopes in 2024.

Looking forward, taking a defensive posture on investments is highly advised. It has been a rough ride for tech investors this past year, but we should expect to see further rough times until we see concrete evidence inflation is abating and/or the administration takes action to reduce tensions in the Ukraine - Russia conflict. As good as tech companies are in their innovation, management, and productivity, they cannot escape glaring macro realities facing the U.S.

As always, please comment on your own views in the comment section below, and “like” the post if you liked it. Also, please share to your friends if you found it valuable!

Disclaimer: BubbleCatcher is published as an information service for subscribers, and it includes opinions as to forecasts on the global economy and its impact on securities linked to economic activity. The publishers of BubbleCatcher are not brokers or investment advisers, and they do not provide investment advice or recommendations directed to any particular subscriber or in view of the particular circumstances of any particular person. BubbleCatcher does NOT receive compensation from any of the companies featured in our articles. At various times, the publisher of BubbleCatcher may own, buy or sell the securities discussed for purposes of investment or trading. BubbleCatcher and its publishers, owners, and agents are not liable for any losses or damages, monetary or otherwise, that result from the content of BubbleCatcher. Past results are not necessarily indicative of future performance. The information contained on BubbleCatcher is provided for general informational purposes as a convenience to the subscribers of BubbleCatcher. The materials are not a substitute for obtaining professional advice from a qualified person, firm, or corporation. Consult the appropriate professional advisor for more complete and current information. BubbleCatcher makes no representations or warranties about the accuracy or completeness of the information contained on this website. Any links provided to other server sites are offered as a matter of convenience and in no way are meant to imply that BubbleCatcher endorses, sponsors, promotes, or is affiliated with the owners of or participants in those sites, or endorses any information contained on those sites unless expressly stated.