A Macro View

A Macro View

What the U.S. dollar is doing and stagflation risks

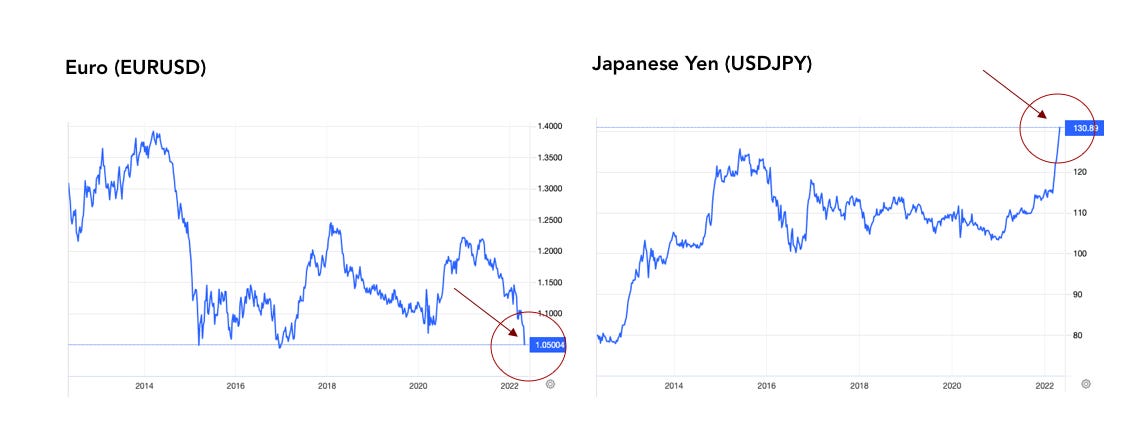

The U.S. dollar is now stronger than it’s been at any point over the last 20 years. The reasons are simple. Inflation pressures are very pronounced in the U.S. while growth pressures are also strong and the labor market remains tight. This means the Federal Reserve will have to raise interest rates at a faster rate than the rest of the world.

Europe and Japan are still suffering from sluggish growth and can’t afford to raise rates at such a rapid clip. The European central bank cannot raise rates at the same rate due to slower growth prospects, weaker consumer sentiment, and a slacker labor market. Likewise, the Bank of Japan recently signaled signs of impending inflation risks, but won’t likely raise rates at the same pace as the U.S.

What this all means is the U.S. dollar will likely continue to appreciate against major currencies for the time being. The mechanics of how this works is simple: massive bond investors will take out loans in a lower-rate country (e.g. Japan) and then lend those funds to a higher-rate country (e.g. the U.S.) en masse, shifting the currency’s value.

So if you’re an American, now is definitely the time to travel. Now is also the time to be earning dollars if you can. A stronger currency makes everything around the world cheaper. It also helps tame U.S. inflationary pressures as American imports become cheaper, which in turn forces U.S. companies to slow price increases in order to remain competitive in their markets.

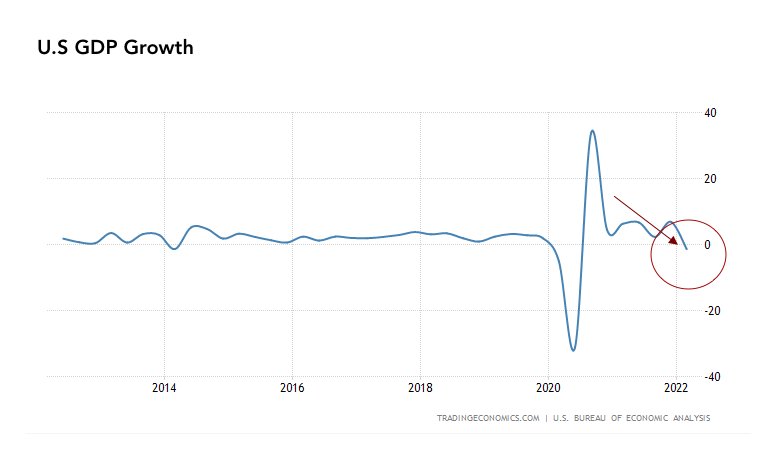

However, now is not the time to party. U.S. growth rates are beginning to dip into negative territory, all while inflation is through the roof, which means we may very well be at the precipice of entering a stagflation cycle. The Federal Reserve is raising rates at a rapid rate, and historically it is not too good at staging a soft landing. We should expect an economic slowdown to occur sometime in the mid to later half of the 2022, with an increasing likely scenario of a recession occurring, all while inflation is occurring.

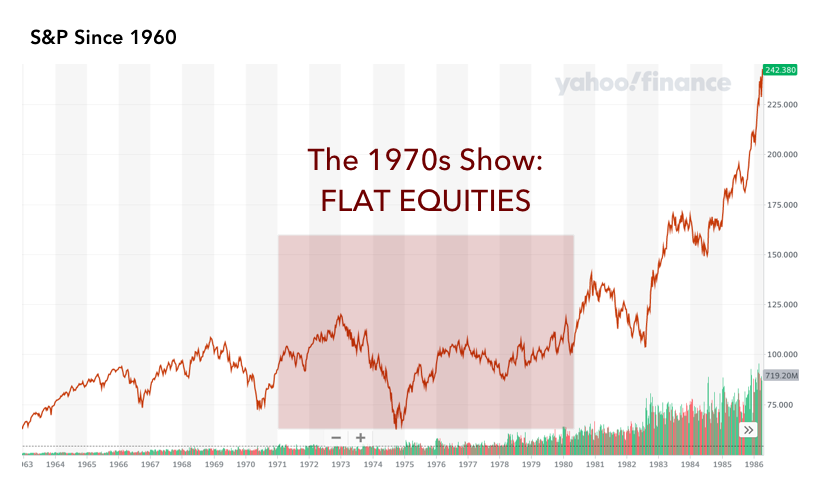

Stagflations are the worst of all worlds in the economic world: painful, impacting all sectors of the economy (consumers, producers, poor and rich), and extremely hard to get out of. The last time we had an extended stagflation was in the 1970s when commercials looked like this:

How awful these commercials look to us illustrates just how rarely extended stagflations occur.

How do stagflations occur? Usually due to a mixture of bad economic policies (too much stimulus that doesn’t bring with it quality growth) along with outside shocks (e.g. the OPEC oil embargo on Israeli allies in retaliation). Today, we have a similar mix of circumstances, with the government having injected huge amounts of money into the economy to combat covid / sluggish growth from the 2008 financial crisis, all while Russia cuts off its oil supply from select markets and supply-chain disruptions push up inflation. We’re essentially back in the 1970s.

The problem is just how long we will be stuck in this state?

Well, a lot of issues need to get addressed to answer this question.

How quickly can the Fed help get inflation under control?

How many more rate increases are needed to convince the world to stop pricing price increases?

How soon can the Russia-Ukraine conflict get resolved?

And how soon can the global economy get supply-chain logistical problems back to normal?

And until we answer these questions, we should expect equities to act exactly as they acted in the 1970s: GOING NOWHERE FAST.

So is it all gloom and doom for the moment? Well, generally speaking, yes. This war doesn’t seem to show any signs of letting up anytime soon.

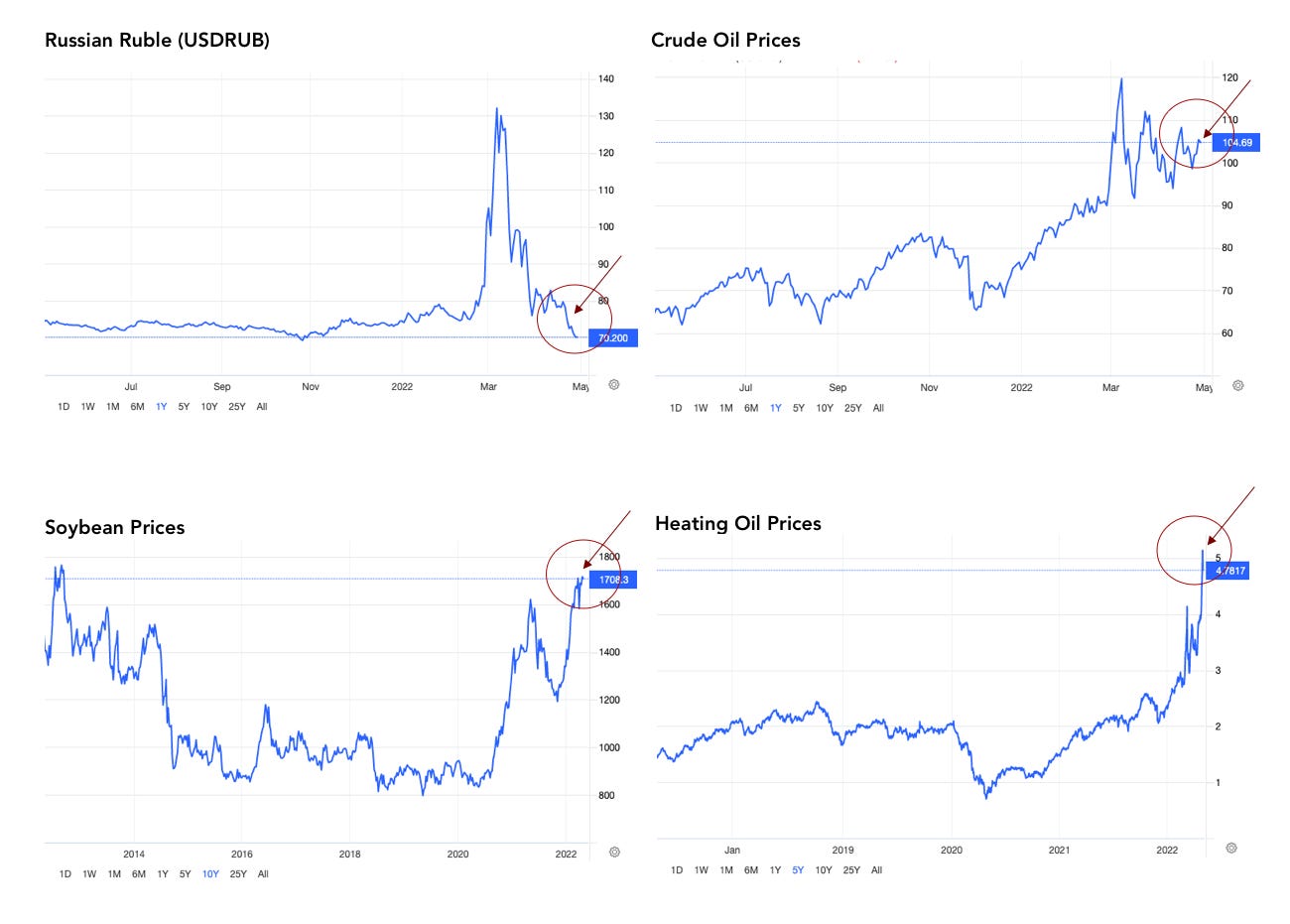

Financial sanctions, which originally seemed likely to choke Russia’s financial ties to the world, seem to now be more bark than bite. The Russian ruble, in fact, has appreciated even further to levels seen even before the crisis started (!), despite the economic pressures Russia’s economy is facing now, suggesting the incentives for Putin to cut his losses in Ukraine are falling fast.

Meanwhile, crude oil prices are fluctuating ever higher, while soybean prices and heating oil prices are quite literally shooting through the roof.

Looking ahead, we should look to a few indicators to tell us when things could start to turn:

inflation data begins to slow to below 8 percent, which would show a reversal of the trend, and / or …

Putin shows any willingness to cut his losses in Ukraine (highly unlikely at the moment)

Disclaimer: BubbleCatcher is published as an information service for subscribers, and it includes opinions as to forecasts on the global economy and its impact on securities linked to economic activity. The publishers of BubbleCatcher are not brokers or investment advisers, and they do not provide investment advice or recommendations directed to any particular subscriber or in view of the particular circumstances of any particular person. BubbleCatcher does NOT receive compensation from any of the companies featured in our articles. At various times, the publisher of BubbleCatcher may own, buy or sell the securities discussed for purposes of investment or trading. BubbleCatcher and its publishers, owners, and agents are not liable for any losses or damages, monetary or otherwise, that result from the content of BubbleCatcher. Past results are not necessarily indicative of future performance. The information contained on BubbleCatcher is provided for general informational purposes as a convenience to the subscribers of BubbleCatcher. The materials are not a substitute for obtaining professional advice from a qualified person, firm, or corporation. Consult the appropriate professional advisor for more complete and current information. BubbleCatcher makes no representations or warranties about the accuracy or completeness of the information contained on this website. Any links provided to other server sites are offered as a matter of convenience and in no way are meant to imply that BubbleCatcher endorses, sponsors, promotes, or is affiliated with the owners of or participants in those sites, or endorses any information contained on those sites unless expressly stated.